Bankruptcy In UK

Bankruptcy is often seen as a last resort, and for many people facing overwhelming debt, it can feel like a frightening word.

Bankruptcy is often seen as a last resort, and for many people facing overwhelming debt, it can feel like a frightening word.

Some debts need to be dealt with immediately to avoid serious consequences. Others, while still important, don’t carry the same urgency.

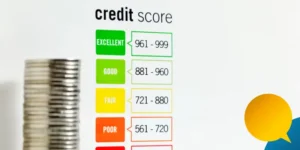

Concerned about your credit rating after entering an IVA? This guide explains what to expect and how to take control of your financial future.